Today’s date is October 12, 2023. It has been exactly 523 days since the collapse of UST stablecoin and we haven’t learned anything about stablecoins.

USDR, a "stablecoin" with a $60m supply, the majority of which is backed by UK real estate, collapsed and lost its peg, rapidly falling to $.50 in a few hours. It was a classic "run on the bank" where the stablecoin had a mismatch in duration between its highly liquid debt and its illiquid collateral.

$USDR, a dollar-pegged stablecoin, is currently trading at $0.53 after a wave of redemptions depleted all of its liquid collateral.

— Bluechip (@bluechip_org) October 12, 2023

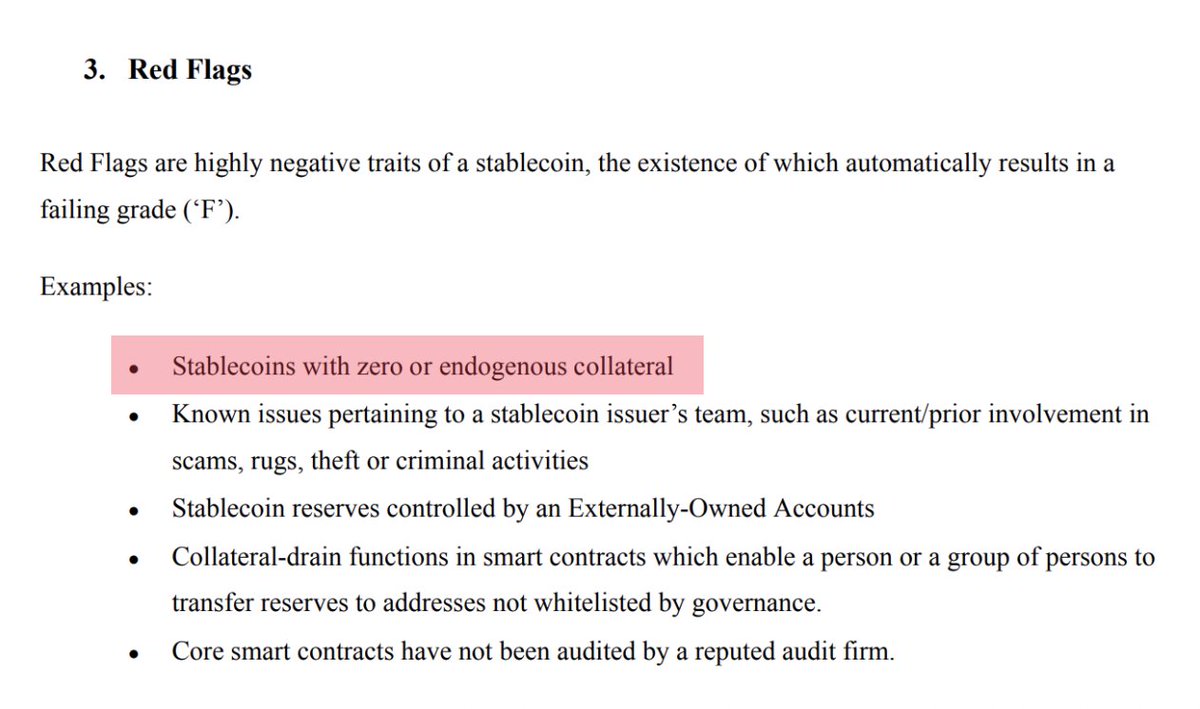

Anyone familiar with Bluechip's rating framework could've predicted USDR's failure. It violates a cardinal rule which instantly earns an F rating.… pic.twitter.com/rEjYaL1etW

The now-deppeged stablecoin is issued by Tangible, a marketplace for buying and selling RWA's. On the platform tokenized versions of real estate, watches wine, and gold could be bought with USDR.

Real USD... Not a Better Money

According to Tangible's docs, "Real USD (USDR) is a first-of-its-kind natively rebasing, yield-bearing, overcollateralized stablecoin, pegged to the US dollar. USDR is primarily collateralized by yield-generating, tokenized real estate."

All USDR is redeemable 1:1 for DAI at all times with a .25% fee. The protocol kept several million dollars in cash to act as a capital buffer and facilitate redemptions.

The depeg occurred when the treasury ran out of $12m worth of DAI it could use to redeem USDR and holders started dumping the token through DEX's to escape. Now USDR holders must wait for the companies treasury assets to be distributed or sold off to cover the collateralization gap.

One of the more interesting parts about USDR is that it's an algorithmic stablecoin with a maximum 10% backing by its governance token.

USDR can be minted using TNGBL or DAI at a 1:1 ratio. The protocol imposes a 10% maximum limit on the amount of USDR generate from TNGBL. The funds collected from the swap are then used to purchase properties in the UK. In their docs, the Tangible team wrote that excess collateral above the CR is used to fund purchases of more real estate collateral. However, the Tangible team told Flywheel that they never did this and all excess collateral was held in reserve.

Bluechip tweeted today that this algorithmic part of Bluechip would immediately have triggered a red flag and earned an "F" rating. They write "As holders lose confidence in $USDR, they will sell TNGBL. As the TNGBL price goes down, USDR's collateral ratio will decrease and holders will further lose confidence."

Real Estate Backing

Tangible provided two reasons for using real estate to back USDR.

First, real estate provides yields. All of Tangible's properties were rentals and generated rent each month that would go to USDR holders through rebasing.

Tangible only buys property in the UK market, providing a yield of 6.39%. Compare this to the short term 1 month UK gilt which is yielding 5.31%.

Second, the team noted "Real Estate price appreciation" over the long term as a driving factor. They said that RE has a "predictable history of appreciation" and that "the average sales price of a house in the United States grew from $27,000 in Q1 1970 to $383,000 in Q1 2020."

They then proceed in their docs to claim that USDR is "Better Money" because it's a "true store of value" because house prices go up over the long term and will protect holders from inflation.

It's like we didn't learn anything from 2008 about illiquid real estate.

At Par on Demand

The biggest lie in crypto is how the three characteristics of money are presented. We've all heard it a million times, money has three properties, Medium of Exchange, Unit of Account, and Store of Value. But these only matter in terms of denomination.

Bitcoin can be money because it retains value and platforms integrate it as a payment option. Same goes for any commodity. Bitcoin can fluctuate 5, 10, 15% daily and it won't diminish its ability to pay as price is relative to a dollar. 1 BTC = 1 BTC as they say.

Dollar denominated debt is held to a higher standard. A USD stablecoin should always be redeemable for either $1 or approximately $1, no matter the circumstances.

If it can't, then it's not dollar-money.

I say approximately because if you accept that privately issued money should have a place in our society, it will always have minimal price sensitivity. Only government issued money, with the full faith of the money printer can be deemed price insensitive.

Stablecoins are facsimiles that track dollars, which FRAX now falls into with the launch of v3. Our stablecoin can be sold for USDC valued approximately $1, but there is no guarantee. The Frax DAO is tasked with maintaining a treasury of highly liquid assets to keep the peg, but circumstances always can change and portfolios battle-plan for the absolute worst.

It's this ten-thousand foot view of a stablecoin that clearly shows the need for it to always trade At Par on Demand.... or at exactly the reference price at all times.

Notably, Tangible was pursuing a growth strategy in Q1 and 2 of this year on Curve. The Llama Risk team raised concerns about their collateral backing. At the same time, Frax DAO voted to increase the CR to 100%. Hameed the FIP author wrote "The costs of being slightly undercollateralized now far outweigh the benefits – especially because it can undermine the perceived safety of FRAX." Frax understood the risk of depeg and how it would signal the end of the protocol.

The lens one must use when viewing stablecoins is "if SHTF and the entire treasury must be sold in a fire sale, how much will I get back?" If it's not "At Par" then the reference denomination is wrong.

Taking into account the assets on Tangible's balance sheet we can make the following assumptions.

- The TNGBL token is "equity-like" and will be worthless when the protocol fails. It cannot add any value to a stablecoin’s backing.

- Both the insurance fund and the POL held by the team will be drawn down to near zero or until redemptions are cut off to preserve remaining collateral.

- When Tangible goes to sell the properties in a fire sale to recoup funds, they may have to sell at a discount to market rates in future unknown market conditions. Additionally, the properties are distributed globally, adding currency risks to their sales.

The question at hand then is what discount to assign the property value. With interest rates at 15 year highs, liquidity has evaporated at these valuations.

Last and final update about USDR after extensive research: the fair value of USDR is ~$0.5 if you take into account that:

— Wismerhill (@0xWismerhill) October 11, 2023

- TNGBL backing is worthless (no liq, no demand)

- Insurance Fund is composed of shitcoins (with vesting!) so 30% fair value

- POL is now 80% USDR

- RE… pic.twitter.com/bNjEwxC8iC

Tangible's Plan of Action

In light of the USDR token depegging, the team has proposed the following steps:

- Asset Liquidation: USDR's current collateral stands at 84%, considering both $TNGBL and the insurance fund as zero. POL was withdrawn from their Pearl staking pool. The company now has approximately $2.4 million in protocol-owned stable assets like DAI, USDC, and USDT. Furthermore, Tangible will liquidate a significant portion of the insurance fund. Proceeds from these liquidations will be made available to users via a redemption process.

- Introduction of Baskets: Instead of a stablecoin, Tangible will offer pools of tokenized real estate, aka property index funds. These Baskets, such as UK Real Estate, will be distributed to USDR holders pro-rate their share of the token. Users can hold the index tokens, earn yield from rent collection, farm them on Pearl, or sell them. If there is no demand for the Baskets, Tangible will begin to liquidate real estate, however, this process will most likely take some months to complete.

- USDR Redemption: Once Baskets are in place, Tangible will initiate the USDR redemption process. USDR will be redeemable in the form of a combination of stablecoins, Basket tokens, and locked TNGBL 3,3+ NFTs. If there's a collateralization gap after this, it will be bridged with TNGBL 3,3+, locked for a year.

Assuming the property can be sold off without a steep discount, each USDR holder will receive:

- $0.052 stablecoins (DAI)

- $0.78 of RE in the form of baskets

- $0.168 of locked TNGBL that receives yield from rents

1/ Tangible announced the redemption plan for USDR, you will receive per USDR:

— Wismerhill (@0xWismerhill) October 12, 2023

- $0.052 of stables

- $0.78 of face-value RE asset (in the form of baskets = REIT)

- $0.168 of locked TNGBL (that receive yield from rents)

They wrote off the insurance fund but will sell the assets. pic.twitter.com/7tQrHeh3NE

There's a reason that every single stablecoin bill in discussion or already passed as law requires all issuers to only hold cash and short term equivalents. Market conditions ALWAYS sour and investors panic. If you don't have enough liquid capital to redeem, depeg/bank runs are inevitable. Illiquid debt increases convexity exponentially. Any time the market perceives a hint of illiquidity, asset prices will be discounted immediately.

At the time of writing this article, the price of USDR is $.53. Even if the team claims the tokens are 84% collateralized, the market knows that it could take months to liquidate the treasury portfolio, discounting it accordingly.

USDR will no longer exist when this process is done. The stablecoin is dead after the run.

It's Only Hubris If They Fail

Let's be clear.... all stablecoins are a form of debt. An extremely liquid, fungible debt instrument in the form of a token. Tangible thought that they could issue millions of dollars of debt 78% backed by real estate with zero duration risk. That somehow a pre-collapse 30% buffer of cash and POL would adequately provide enough liquidity in case of a run.

Today's events have been repeated untold number of times in TradFi and it's telling about the project when the claim "Elements put in place to protect the customer were too easily manipulated to attack the protocol." This is just not true. nor is it true that Tangible "tried something new." The team intentionally issued redeemable liquid debt tokens against illiquid assets. Tangible marketed their "stablecoin" to unsuspecting non-institutional users who bought their marketing lingo.

What's frustrating about the collapse of USDR was the risks were documented by the Llama Risk team, who wrote:

In conclusion, Tangible has built several mechanisms that support the peg of USDR. They have conceptualized a promising method (pDAI) to assure that USDR holders can always redeem USDR for something of equal value. However, most measures are still new, and not battle-tested, and some are fully centralized (e.g. real estate liquidations). Especially in the case of a bank run, it's questionable whether USDR can hold its peg. Moreover, the project introduced multiple dimensions of additional complexity and potential weaknesses through its wUSDR token and Multichain integration. These factors do not contribute to the safety of USDR’s peg stability.

Yet here we are today discussing the failure of yet another “stablecoin.” It’s frustrating because these events are exactly what regulators and anti-crypto lawmakers reference when drafting draconian rules and laws. Tangible’s implosion adds fuel to the anti-crypto lobby as exactly why our industry should be shut down.

It's time to dispel any idea that a stablecoin can be backed 1:1 with anything other than cash or short term equivalents. Real estate is a fine collateral, but allowing 100% LTV loans against the equity of a home in the form of a stablecoin is clearly disastrous.

At Frax, we're committed to building a robust stablecoin ecosystem with as minimal risk exposure as possible. In the latest v3 rollout, Frax is also using RWA's to provide yield to the DAO, however, only the most liquid assets with the shortest duration are allowed: T-Bills, Overnight Repo, USD in a Fed Master Account and select money market funds. Nothing else.

Otherwise you end up with a Thanksgiving Turkey growth chart. 1:0 in a a matter of minutes.